2022 started out on rough terrain as volatility is part of the game. When you think about it, volatility is the risk investors take on when investing in the capital markets. Of course, different securities and asset classes have different volatility characteristics. For example, stocks have historically been more volatile than bonds. Without volatility, there is no risk and investors would get risk-free returns. We call that cash and cash equivalents.

2022 started out on rough terrain as volatility is part of the game. When you think about it, volatility is the risk investors take on when investing in the capital markets. Of course, different securities and asset classes have different volatility characteristics. For example, stocks have historically been more volatile than bonds. Without volatility, there is no risk and investors would get risk-free returns. We call that cash and cash equivalents.

When volatility happens, people tend to entertain market timing strategies in lieu if their long-term investment strategies. In essence, the purveyors of market timing wares infer superior investment skill by timely exiting and entering investment markets. The reality is numerous academic research studies have proven market timing is not a fruitful endeavor.

Most research on this subject compares different market timing strategies to a strategic investment strategy. In summary, all have come to the same conclusion that strategic strategies outperform. There have been a few studies attempting to quantify needed market timing success to equal strategic strategies. These few studies have generally concluded that a market timer has to be 70% – 80% correct1,2. For context, the best professional money managers get 52% – 55% of their investments correct. This is slightly better than flipping a coin. Only the rare professional money manager gets as high as 60%, which tends to be short lived.

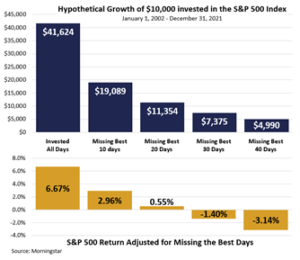

To complicate things, the best days tend to be clustered with the worst days as the best days rebound from the worst. Generally, market timing efforts signal “sell” after a decline has begun, which also means buying after the rebound commencement. A close look at missing the 10, 20, 30 or 40 best days out of a 20-year period drastically reduces returns.

These studies and statistics don’t consider real world items such as trading costs, taxes, price slippage, etc. So, market timing with lagged triggers has to be correct more often that the best money managers, and market timing also has to overcome the added real-world costs.

When the inevitable market decline occurs (it’s a when, not an if), it’s normal to feel the urge to sell. This is when an investment plan works best in your favor. An investment plan helps you stay disciplined and avoid the big mistake. With foreknowledge of human reactions, you are now better prepared to deal with volatility when it rears its head.

1William Sharpe “Unlikely Gains from Market Timing” Financial Analysts Journal (March-April 1975)

2 Jimmy Hillard “Timing versus Buy and Hold: A Model for Determining Predictive Accuracy Required for Superior Performance” Auburn University (2011)

The opinions expressed are those of Heritage Financial and not necessarily those of Lincoln Financial Advisors Corp.

CRN-4209619-012022

Recent Comments