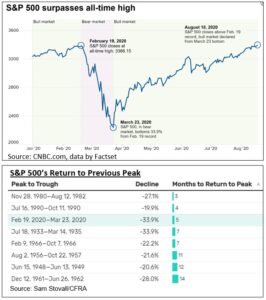

This week witnessed the S&P 500’s return to its previous peak. The previous peak occurred on February 19, 2020 just before the COVID economic shut down and the oil market disruption. The following bear market (defined as a decline of 20% or more) declined 33.9% in just over a month… one of the fastest in history.

Since the nadir on March 23rd, the S&P 500 experienced one of the quickest recoveries in history. In fact, the two quicker recoveries (in 1982 and 1990) did not reach the depths of the COVID induced bear market. As such, the current recovery can be considered the most assertive recovery on record.

Admittedly, the COVID decline was not a typical bear market. As mentioned in previous letters, the COVID decline and accompanying recession were not based on normal consumer exhaustion or excessive business dynamics. It was based on a globally sweeping pandemic prompting drastic measures. Hence, consumers and businesses were primed for any hint of normalcy.

Market performance is not as evenly handed as it appears. A handful of stocks (especially Facebook, Amazon, Netflix, Microsoft, Apple and Google (FANMAG)) were the primary drivers of the S&P through mid-July. The few stocks (mainly in technology, communication services and consumer discretionary) accelerated the S&P 500’s recovery. Limited market drivers (both in stocks and sectors) are referred to as a “narrow market” and not considered healthy. This is also why domestic Large Growth stocks have trounced almost all other classes. Fortunately, this fate has turned as consumer consuption, busness semi-reopening and economic measures have begun to impact a broader array of asset classes and sectors over the past month.

As colleges commence their Fall semesters, there are 32 COVID vaccines in various human trial phases. A record in terms of vaccine development. No doubt caution is still warranted. But clearly, the stock market is taking cues that an improving economic situation is looking brighter.

¹ https://www.nytimes.com/interactive/2020/science/coronavirus-vaccine-tracker.html

CRN-3209931-082020

Recent Comments