There are many ways to evaluate stocks. All approaches can be boiled down to two primary styles. We term these “growth” and “value” investing. Both styles and their permutations can be implemented among differently sized companies (small, mid and large caps) as well as domestically or abroad. The distinguishing factor is how a money manager views the presented opportunities and pursues returns.

Growth investing seeks to invest in companies that are growing faster than the overall economy or faster than the overall stock market. Growth investing tends to involve analysis of current and accelerating trends which will hopefully translate into higher profitability. This would be akin to buying the latest fashion, risking that the fashion may go out of style quickly. The risk is that the trend may not materialize as expected, making growth company stock prices vulnerable.

Value investing generally seeks stocks which may be undervalued. Value investing tends to require strict fundamental analysis of the underlying company. This would be akin to buying a winter coat in summer, risking that you may not need the coat when winter arrives. The risk is that the low value of the stock is warranted and stays depressed for a prolonged period of time.

When it comes to portfolio design, portfolio architects generally develop portfolios that have exposure to both. The reason is that it is extremely difficult to determine, if not impossible, which style outperforms in the near-term. Additionally, exposure to both styles reduces the risks of either style.

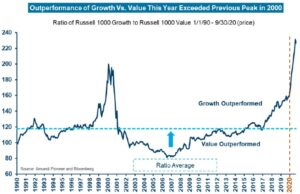

It is important to monitor the relative difference as it could offer insight into market dynamics. Since 2017, growth has taken the lead by a sizable margin. Even more interesting is that the growth style has exploded relative to value investing during 2020. Many often refer to the “go-go 90s” when talking about such growth investing disparities. However, the disparity during 2020 has surpassed even the “go-go 90s.”

Is there an opportunity or an arbitrage to be captured? Possibly. Yet, there is no telling how long the disparity will last or how the disparity will end. Disparity could quickly disappear like the “tech wreck” of the early 2000s or it could simply evaporate over a period of years, which is more typical. It’s important to recognize the disparity may not be as vast as it appears since the growth style is being driven by a handful of stocks.

Growth and value styles are like a yin and yang. They complement each other and both are part of the whole. The disparity may seem exaggerated, but it is important to maintain exposure to both styles.

CRN-3296812-102220

Recent Comments