Now that the election is behind us, investors will attempt to evaluate the political impact on financial markets. Over the past few months, there have been copious prognostications and guesses about the political influences on financial markets. How will the policies of one candidate or the other change investment markets? Will interest rates go up? If so, by how much? What are the spending initiatives and how will they impact industries? The list of questions can go on at infimum.

Much to pundits’ dismay, elections seldom have a lasting impact on financial markets. Pundits often like to create controversy where there is none. Talking about issues is partly how they generate earnings, even if the topics are inconsequential. What better way than to measure stock market performance then by political party.

There seems to be defined start and end dates… or is there? Some would measure the time between inaugurations as these points. However, the stock market is a discount mechanism. So, maybe the more appropriate start and end dates would be election dates, or when a victor is declared.

Another decision is when to begin the evaluation. 1929, 1932, 1945, or 1980? Changing the historical yardstick often changes the conclusion. The saying, “torture the numbers long enough and they’ll confess to anything,” seems to apply. None of this considers policy objectives, debate and compromise, passage, implementation latency or Congress’ control of the purse strings.

Let’s boil this down to what really matters. Irrespective of the victor (still unknown as of this typing), the most important factor effecting the financial markets is the state of the business cycle. From this point of view, the landscape looks very appealing. The next economic segment is recovery and expansion. Fellow citizens are getting back to work. Incomes are growing. People are spending money. Businesses (for the most part) are earning revenue with a high percentage of earnings surprises. (Earnings Surprises are companies’ earnings higher than expectations.) This is not to say we are clear of the COVID struggle, and certainly, some industries have been impacted more than others. But in aggregate, the view is improving markedly.

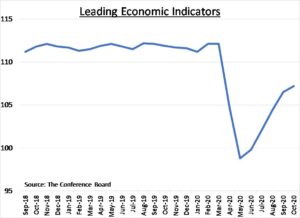

The best representation of things to come is the Leading Economic Indicators (LEI). The LEI is a very good indicator of economic activity in the near future. The trend is what matters. There is little doubt the LEI is pointing to better days ahead.

CRN-3316453-110420

Recent Comments